Are you ready for a fun talk? Let’s talk workers’ compensation! According to the National Council on Compensation Insurance (NCCI), the private carrier combined ratio for workers’ compensation was recently at 87 percent. This marks the seventh consecutive year of underwriting profit. While other lines of Property Casualty coverage have seen rate increases, experts continue to predict that rates will remain stable with some rate decreases and others may have minimal increases.

While that is good news, I think it’s important to be aware of a few areas that could cause pressure to the workers’ compensation rate. No doubt increased widespread labor shortages, increased mega claims, and medical inflation are three of those contributing areas.

Qualified Worker Shortages

If you aren’t experiencing this within your organization, congratulations!

The U.S. Bureau of Labor Statistics confirmed there were more job openings available in 2021 than in the previous 20 years. Some economists are predicting the labor shortage to continue as the pandemic influenced many baby boomers to retire early.

Unfortunately, because of these labor shortages, many companies have had to look to an inexperienced worker and provide on-the-job training. Other organizations have had to reduce their job hiring requirements. As you can imagine, these practices come with multiple workers’ compensation risks.

A recent survey by the Golden Triangle Business Roundtable found employees with less than five years of experience contribute to 43 percent of workplace injuries. Knowing this, organizations need to really focus on new employee training. It’s important to also be aware that relying on current employees to fill gaps and work longer shifts may result in fatigue and increased claim frequency.

Mega Claims

A mega claim is defined as a large insurance claim totaling $3 million or more in incurred losses. In the scope of workers’ compensation, these claims typically stem from employees experiencing severe and possibly permanent injuries on the job. The NCCI reports that mega claims have reached a 12-year high, increasing in both frequency and severity.

Medical Inflation

Are you tired of talking about inflation? What about medical inflation? I recently had the opportunity to attend a training on medical inflation and how it impacts our clients’ healthcare costs. It made me think about the trend we will see on workers’ compensation.

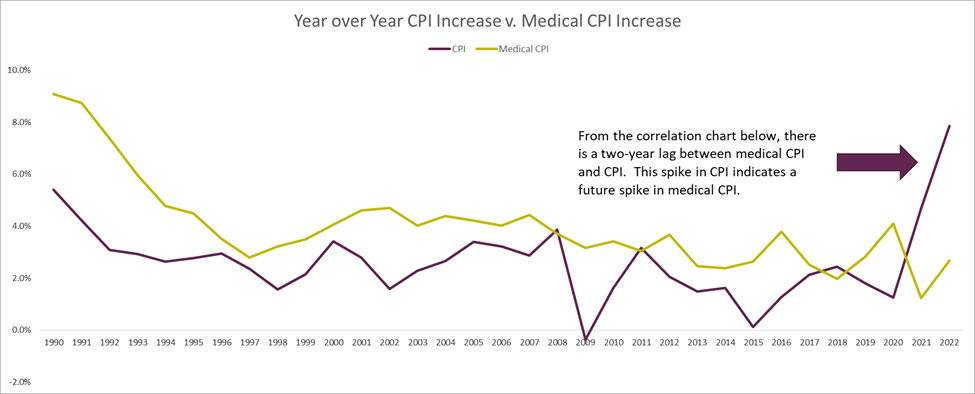

Here is a chart that got my attention from a presentation our Employee Benefits team recently gave based on stats from both the U.S. Bureau of Labor Statistics and Federal Reserve Bank:

This chart doesn’t look so bad, and clearly the Consumer Price Index (CPI) is seeing the spike with inflation, but here is what I learned and something to be aware of in future strategies: the highest correlation between CPI and medical trend indicates a two-year lag. Based on the above chart, one could anticipate increases in the 2023 and 2024 medical trend.

Combatting Workers’ Comp Issues

It’s important to think about these future trends, but there are things your organization can do. No loss is the best trend. Strong hiring practices, training of employees, wearable technologies, and an increase in focus on safety culture are just a few ways you can set your company up for success.

Our team stands ready to help you reduce loss and keep your workforce safe. Let’s get started!