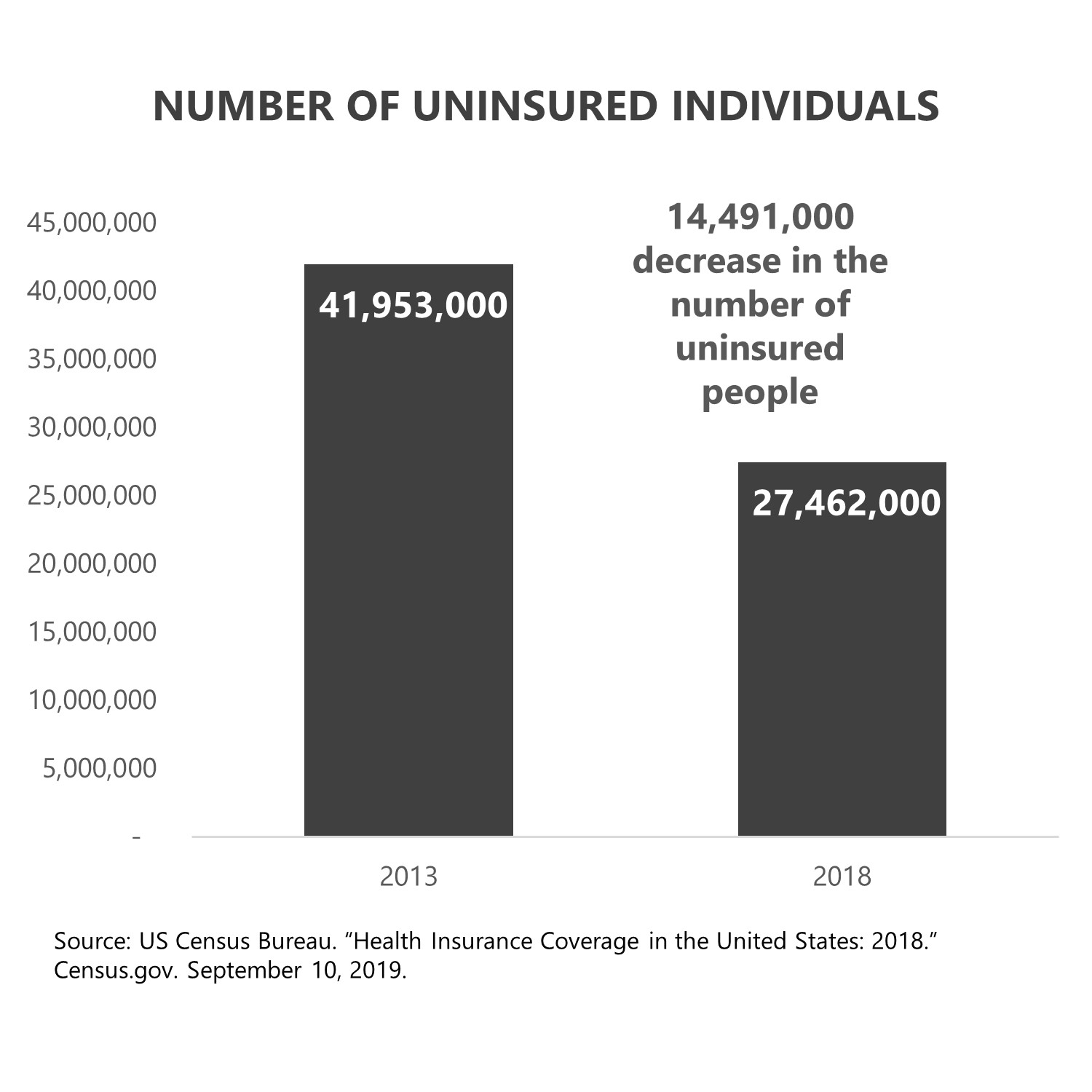

A major goal of the Affordable Care Act (ACA) was to decrease the number of uninsured people in the US. The coverage expansions were implemented in 2014. Between 2013 and 2018, the number of uninsured people in the US dropped from over 41 million to just over 27 million. (1) Supporters of the law can claim that the number of uninsured people has dropped by more than 14 million people. Those who believe the ACA did not go far enough will point out that more than 27 million people in the US still lack health insurance coverage. So, who are these 27 million, and why do they lack health insurance coverage despite Medicaid expansion, a new subsidy system, and a mandate that everyone have coverage?

People

People

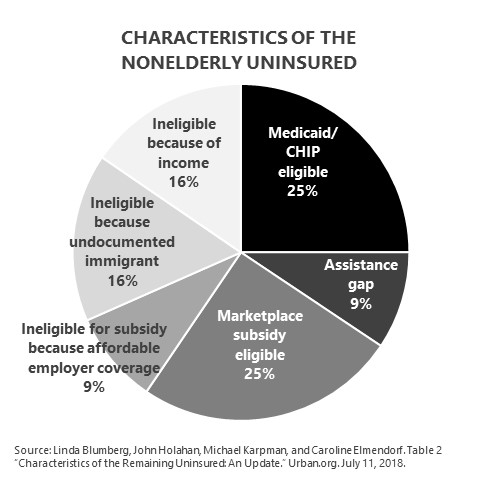

A 2018 report funded by the Robert Wood Johnson Foundation and the Urban Institute examined the characteristics of the nonelderly uninsured population. The report provides the following granular insight regarding uninsured groupings by rationale. (2)

- Medicaid/CHIP Eligible—Over 7.5 million uninsured individuals are eligible for either Medicaid or CHIP. This group includes those who are unaware of their option for free health insurance coverage, have other barriers to enrolling in coverage, or are purposefully choosing to remain uninsured.

- Assistance Gap—This group of 2.8 million includes adults in states that have not expanded Medicaid eligibility and who earn less than 100 percent of the federal poverty level (FPL). Marketplace subsidies are not available for individuals who earn less than 100 percent of the FPL; therefore, these low-income individuals do not qualify for Medicaid or for a Marketplace subsidy. This group is particularly economically vulnerable.

- Marketplace Subsidy Eligible—Over 7.5 million people are eligible for a subsidy in the Marketplace but have chosen to not purchase health insurance. The most common reason cited for this decision is that they still deem coverage unaffordable. The average subsidy covers 86 percent of the total health insurance premium, and the average per-person net premium is less than $3 per day.

- Ineligible for Subsidy Because of Affordable Employer Coverage—Over 2.6 million people have access to affordable health insurance through their employer but have chosen to not purchase coverage. “Affordable” is defined as a plan that meets the minimum essential coverage requirements and costs the employee no more than 9.86 percent of household income for single coverage. A worker who is eligible for affordable coverage is not eligible for a Marketplace subsidy. Family coverage does not have an affordability definition. The definition using household income and single coverage creates a potential gap for employees with family members. Single coverage might be “affordable,” but family coverage may not be. Family members are not eligible for a Marketplace subsidy because the individual coverage for the worker is “affordable.”

- Ineligible Because of Undocumented Immigrant Status—The ACA specifically did not expand coverage to undocumented immigrants. Hospitals are required to provide emergency care to anyone who needs it, without regard to citizenship or immigration status. For purposes of The Voter’s Guide to Healthcare, I will not address this population. I view this as more of an immigration issue, and my upcoming book is intentionally not The Voter’s Guide to Immigration.

- Ineligible for Marketplace Subsidy Because of Income—Marketplace subsidies are available to people who earn up to 400 percent of the FPL. Over 4.6 million Americans have decided that health insurance does not represent enough value to purchase, even though they earn more than 400 percent of the FPL.

Uninsured Recap

- The US, the country with the world’s largest economy, has more than 27 million people who have no health insurance.

- The ACA reduced the number of people without health insurance.

- Public programs that provide free or heavily subsidized coverage are available to many of those who choose to be uninsured.

- Gaps between programs create an assistance problem for some of the uninsured.

What’s Next?

The bottom line is that the US is the only economically developed country without a formal universal healthcare system. This is a social-justice issue that cannot be politically ignored. Several states have introduced ballot initiatives to create universal coverage in their state. Finding the money within each state to fund the initiatives has been too much to overcome so far. Expect left-leaning states to continue to explore state-based efforts to achieve universal coverage if the federal government is unable to do so.

“Healthcare is a right” signs will be common in presidential campaign stops. If our country believes healthcare is a right, the question becomes whether this right has a corresponding responsibility—the responsibility to pay for it. The balance between the right to have something and the responsibility to pay for it, as an individual or as a country, is the essence of the political healthcare debate.

Closing

After the last several blogs that I’ve posted, here’s what I want you to know about the people involved and insurance coverage. If you had 100 people in the room representing a cross-section of the American population, the group would look something like this:

- 49 of them get their coverage through their employer and are concerned about rising premium costs and increasing out-of-pocket costs;

- 22 of them are covered by Medicaid, and more are joining the group every year;

- 14 of them are covered by Medicare, and more are aging into the group every year;

- 3 of them buy individual coverage with no government or employer assistance, and they face the full force of health insurance costs on their own every month;

- 3 of them get subsidized Obamacare; and

- 9 of them have no health insurance at all.

Thoughts? Questions? I’d love to hear from you on this topic!

Next week, I’ll take a look at a little something I call “Underwronging and the Health Wars.” Be sure to tune in. And, if you haven’t already, I encourage you to sign up for our “Insiders’ Club” where you’ll be notified when I release new information AND receive a FREE copy of my book “The Voter’s Guide to Healthcare: A non-partisan, candid, and relevant look at politics and healthcare in America” when it’s available.

Sources

- US Census Bureau. “Health Insurance Coverage in the United States: 2018.” Census.gov. September 10, 2019.

- Linda Blumberg, John Holahan, Michael Karpman, and Caroline Elmendorf. “Characteristics of the Remaining Uninsured: An Update.” Urban.org. July 11, 2018.