On September 24, 2013, political enemies President Barack Obama and Senator Ted Cruz, who rarely agreed on any subject, made almost identical statements related to employer-sponsored health insurance. President Obama referred to employer-sponsored health insurance as a “historic accident,” while Senator Cruz referred to it as a “historic anomaly.” Both believed the employer role in healthcare was misplaced, with President Obama believing the government should play a bigger role in replacing the employer, and Senator Cruz believing the consumer should replace the employers’ power in healthcare. Either way, both believed the employer-sponsored system was wrong and broken. So how did employers get themselves into the health insurance business, and what is their appropriate role?

Employers entered the health insurance arena as a response to the World War II wage freezes. The government was worried about hyperinflation and instituted wage freezes to slow inflation. Employers looked for non-wage alternatives to attract and retain workers, and health insurance became a tax-preferred alternative to compete for labor. The WWII wage freeze obviously ended, but the tax-preferred incentive to obtain health insurance through your job has continued without interruption.

With approximately 159 million people under age 65 covered by employer-sponsored health insurance, more Americans get their health insurance coverage through their employer than through any other method. The total number of people covered by employer-sponsored health insurance has not changed significantly since the ACA was implemented, and the Congressional Budget Office (CBO) is forecasting the number of Americans receiving health insurance through this system will remain at the same 159 million 10 years from now. This projection is in spite of a federal mandate to offer coverage to full-time employees, cost increases that continue to outpace inflation, and the launch of a subsidized individual health insurance exchange system that guarantees coverage with full preexisting-condition protection.

Participation and Mandates

The ACA mandated that large employers, defined as having 50 or more full-time employees, must offer their full-time employees affordable, comprehensive health insurance coverage. Affordable means single coverage can’t cost more than 9.86 percent of household income in 2019. Not offering health insurance results in a penalty of $2,320 per full-time employee, but there is a penalty-free exemption for the first 30 employees. Yes, 30 employees — you can’t make this stuff up. A large employer who chose to not offer health insurance to its employees would pay a penalty on the total number of employees less 30.

If the plan is offered but doesn’t meet value and affordability requirements, employers face an annual penalty of $3,480 per full-time employee who receives a subsidy through the Marketplace. Individual tax penalties have been reduced to zero, employers with fewer than 50 employees have no requirement, but large employer penalties are still in place.

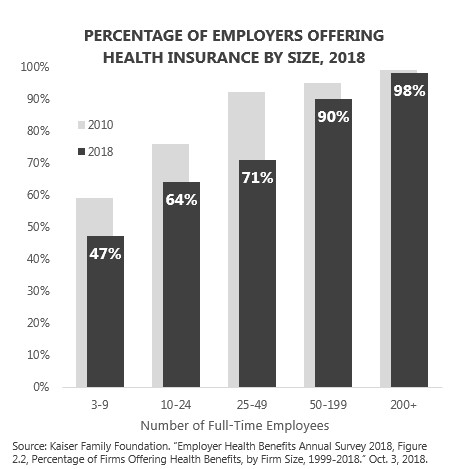

The mandate did not create an increase in employer-sponsored insurance coverage. The prevalence of employers offering health insurance has decreased since the ACA was signed in spite of the mandate. The significant decreasing prevalence in offering health insurance to employees has occurred in small employers who are exempt from the mandate. The likelihood of offering health insurance to employees increases as the number of employees increases. Ninety-eight percent of employers with more than 200 full-time employees offer health insurance to their employees. The mandate for large employers has helped keep them in the health insurance game, but it has not increased the health insurance offer rate and it has not stimulated positive growth in offer rates in smaller employers.

Cost Increases

The average total employer-plus-employee cost for employer-sponsored health insurance for a family of four in 2018 was $28,166. Let’s put this number in perspective. For this amount, you could have paid for a full year of undergraduate pre-med tuition and fees at the University of Texas, bought a brand-new Honda Fit at full sticker price, blown $800 on a Tory Burch purse, and still had enough money to take a friend to dinner and margaritas at Chuy’s in Austin to celebrate. Remember, this healthcare cost isn’t a one-time expense; it is like paying for college and buying a new car every year!

Costs continue to rise faster than wages — and faster than the economy — for both employers and employees. A disproportionate share of the increasing cost is passed through to the employee. The combined per-paycheck and out-of-pocket expenses for employees have increased 109 percent between 2007 and 2017 according to the Milliman Medical Index.

The ACA did little to lower the cost of health insurance for employers or their workers. In fact, a case could be made that the Medicare cost-shifting, coverage mandates, Obamacare Marketplace pricing disasters, and industry fees turned the employer-sponsored insurance market into the naïve tourist who became easy prey for professional healthcare pickpockets.

Reluctant Employer Responsibility

With more Americans receiving their health insurance through their employer than through any other source, employers play a vital role in funding and administering health insurance. Employers pay the majority of the cost and provide important enrollment, billing, and communication services. They take on these financial and administrative roles because health insurance is an important employee attraction and retention tool. For many, health insurance is more than an employee expectation, it is a required element of compensation.

The individual health insurance market rates vary by age according to a regulated tier structure. The health insurance rates in the employer market are the same for every employee in a company without regard to age. Insurance companies use different methodologies and different information to determine the required premiums based on the number of eligible employees.

- Small Group (<50 Full-Time Employees) — The ACA regulates the rating methodology for groups of less than 50 employees. The rates are determined by the plan design, network, age mix, and geographic location of the covered individuals and are not based on health status or claims history.

- Large Group (50 or More Full-Time Employees) — The majority of Americans who receive their health insurance through a large employer are covered by some form of self-insurance. Employers with 100 or more participants must file an annual Form 5500 report. Department of Labor analysis of these filings shows that 83 percent of participants receive their health insurance through a self-insured plan. Self-insured means the employer funds claims on an on-going basis rather than paying premiums to an insurance company. The employer bears the claims risk. They save money if claims are lower than expected, but they spend more if claims exceed expected levels. In a self-funded health plan, the employer is actually the insurance company.Fully-insured refers to health plans that pay fixed monthly premium rates to insurance companies based on monthly enrollment. The rates are determined on an annual basis. Health status, claims history, and known pre-existing medical conditions are primary drivers of the required insurance rates. There are no pre-existing medical condition protections for the employer rates. The individual who has a pre-existing condition cannot be denied coverage or charged more, but the employer who covers them bears the financial burden whether they are self-funded or fully-insured.

Community rating in health insurance means all participants pay the same premium for the same coverage without regard to individual health status or claims history. Experience rating means the claims experience determines the future premium cost. It might be better if we redefined the terms and considered each large employer as community rated because the cost of insurance is based on your unique community, and the community is made up of the employees and their covered family members. If you work for a company with more than 50 employees, the cost of health insurance for your company and for you is determined by the health of your coworkers and their covered family members. Would an understanding of this reality cause people to look at their co-worker community differently? Health insurance cost increases and benefit cuts are not driven by insurance companies, they are actually created within your employee community.

Let’s use car insurance to shed light on the health insurance reality. If car insurance was an employee benefit, then the cost of car insurance for every employee inside the company would be the same. The car insurance would also be available to spouses and children. Bad drivers would be mixed with good drivers. Those who drove more expensive cars, had much longer commutes, and had more frequent accidents would pay the same as those with less expensive cars and no accidents. Drivers would enjoy pre-existing automobile protection! Car insurance would also be administratively easier because the employer would deduct the cost from the paycheck, and the cost would be tax-deductible.

Let’s assume the employer is self-funded for car insurance for the employees. More accidents means more expense for the employer. Let’s assume the rate of inflation for car insurance is more than double the rate at which the employer can increase the prices for its products and services. To add to the equation, the federal government passed legislation that required large employers to offer car insurance or pay a penalty to not offer. What action does this employer in our theoretical car insurance mandate world do? Remember, they can’t charge employees who have accidents or speeding tickets more.

The likely actions of the employer would be to shift car insurance premium increases to employees to manage the company expense and increase deductibles so participants would pay more when they had an accident. In addition, they would eventually look for ways to try to encourage their employees and covered family members to be better drivers so they would have fewer accidents and that those accidents would be less severe. They would be forced to implement automobile wellness!

The car insurance story is not real, but it’s applicability to health insurance is hauntingly accurate. This is exactly what has happened to employers and their employees. The large employers are mandated to offer coverage, the rating system links cost to the employee and family community, the participants are protected from pre-existing condition penalties, and the employer is left to try to figure out how to make people healthier to maintain affordability for the company and the workers.

Because employers own the risk for the health and resulting claims in their covered population, they find themselves reluctantly tied to sometimes invasive wellness and care intervention programs in an attempt to control this ever-increasing business expense. I refer to much of today’s corporate wellness as wellness scavenger hunts. Employees and their covered spouses must check the boxes of their wellness plan requirements or pay a per-paycheck penalty throughout the following year. I did not really like scavenger hunts as a child, and I don’t really like the scavenger hunt approach to wellness as an adult.

Just because I don’t like the current approach to wellness does not mean I don’t believe employers are in the best position to positively influence risk and population health. My company’s wellness required me to get a colonoscopy when I turned 50. I am familiar with the cancer screening guidelines and knew the procedure was clinically appropriate. The employer requirement gave me strong financial incentive to follow through on the test I knew I needed. Thankfully, my colonoscopy revealed no signs of cancer. Others my age in our company have had pre-cancerous polyps discovered and removed. In our company, we believe this type of financial incentive for personal wellness and screenings is appropriate. Other employers feel that employee wellness is none of their business. Employers must individually determine their role in their employees’ health and wellness. Frustration over uncontrollable cost increases, increasing administrative burdens, and employee relations damage from annual health insurance changes has some employers looking for an exit door.

What’s Next?

Employers play a critical role in the financing of healthcare. More Americans get their health insurance through their job than through all other pathways combined. The healthcare system does not financially work without this massive source of money. Continued cost increases will drive employers to explore alternatives to the current options. These options could include public plan options, Medicare indexing, or 401(k)-like defined-contribution plans, where employers escape their current underwriting community cost burden.

I know I covered a lot, but I’d love to hear your thoughts on this. Let me know!

Next week, I’ll take a look at the ABCs of the Affordable Care Act and what it means to you. Be sure to tune in. And, if you haven’t already, I encourage you to sign up for our “Insiders’ Club” where you’ll be notified when I release new information AND receive a FREE copy of my book “The Voter’s Guide to Healthcare: A non-partisan, candid, and relevant look at politics and healthcare in America” when it’s available.