The year was 2003, and I was working with a Fortune 500 company in Austin, TX, that would be the first large employer (over 10,000+ covered employees) to launch a consumer driven health plan (CDHP). The savings the company realized from the federally mandated high deductibles would be redistributed in the form of Health Savings Account (HSA) dollars so employees and their dependents could be better stewards of their own money. Employees loved that the money the company contributed in the HSA and their own deposits was theirs to keep, and they would not lose it at the end of the year (FSA) or when they left the company (HRA).

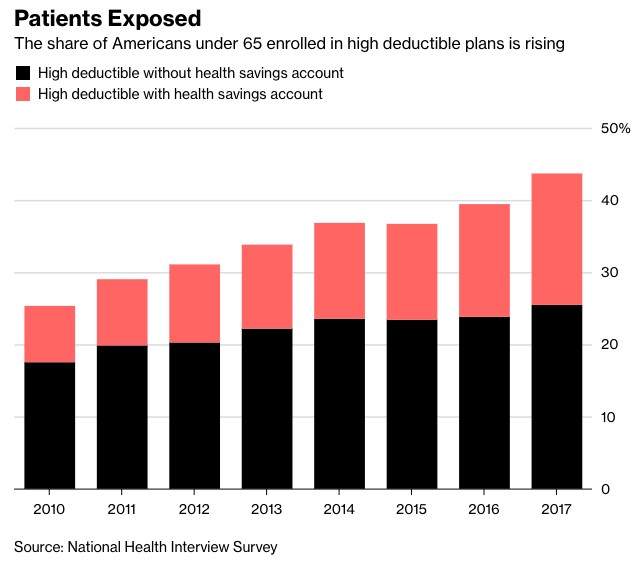

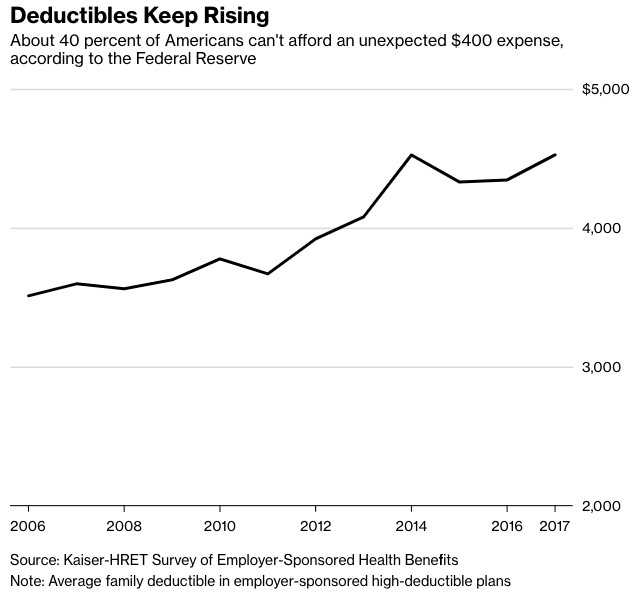

As we flash forward to the 2019 healthcare marketplace, average deductibles for employer health plans have tripled, and there are growing signs that many patients are foregoing prudent care and treatment. There are almost 40 percent of large employers that offer only high-deductible plans, up from 7 percent in 2009, according to the National Business Group on Health. The Federal Reserve has cited that 41 percent of Americans are unable to pay a $400 surprise emergency expense without having to borrow or sell something to make ends meet. While many of my competitors will gladly sell you more accident or condition-specific products full of commissions, gap insurance is not the panacea for our broken sick-care system.

As reported in Bloomberg, some big companies are sitting up and taking notice. “We all thought high deductibles are going to drive people to get involved — ‘skin in the game,’” Jamie Dimon, the Chief Executive Officer of JPMorgan, said in early June. Instead, “they didn’t get the surgery they needed, when they needed it, because they can’t afford the high deductible in one shot.” JPMorgan is effectively eliminating deductibles for workers making less than $60,000 a year. CVS also went to a qualified high-deductible health plan (HDHP) with an HSA and converted all 200,000 employees and their families from traditional preferred provider organization (PPO) plans. Their Chief Medical Officer found their own employees started to stop taking needed medications — and they are in the pharmacy benefit management and retail and drug business!

Another challenge for consumers under employer-based plans has been the great cost shift. With price tags for private insurance plans running 150-300 percent of what a hospital would charge Medicare or Medicaid patients, providers continue to ask private plans to shoulder more of the burden.

While it is not a cure-all, we are beginning to see alternative health plan (AHP) designs that forego large deductibles toward burden sharing at the point of service that direct towards providers with quality outcomes. ACAP Health’s proprietary health plan that marries the best attributes of healthcare navigation with evidence-based clinical interventions is called SimplePay Health. ACAP is a wholly owned subsidiary of Holmes Murphy. A select group of employers have been invited to beta-test this new health plan that can replicate the valuation level of traditional plans based off our in-house actuarial modeling platform. We believe the marketplace will begin to embrace doing away with confusing deductibles and out-of-pocket calculations in favor of a simple, straightforward, all copay-based approach that lets employees know what their share is before they get treatment.

Our market leaders will be sharing more in 2019, and we look forward to working with leading employers to disrupt a system in need of change. Stay tuned!